Unified Risk Management for Prefab Housing

A Protected Cell Company accelerating the manufacturing, installation, and renting of Prefabricated Homes and ADUs—serving General Contractors, Property Owners, and Tenants across three distinct market segments.

Our Mission

To create a unified risk-management and financial suite that accelerates the manufacturing, installation, and renting of Prefabricated Homes and Accessory Dwelling Units (ADUs)—addressing the housing crisis through innovative insurance structures that protect all stakeholders in the prefab ecosystem.

📺 Learn More

Video Overview

Podcast Episode

The Ecosystem

General Contractors

GCs specializing in prefab installations pool risk through captive membership, smoothing cash flow and protecting against innovation risks.

Property Owners

Operators of prefab villages (student housing, trailer parks) offer in-house renter's insurance to tenants through integrated portals.

Homebuyers & Tenants

ADU buyers access bundled financing and gap coverage. Tenants in covered properties get seamless renter's insurance enrollment.

GC Innovation Insurance

Incentivizing General Contractors to specialize in prefab installations by protecting them against the fortuitous risks of adopting new techniques.

💡 The Corporate R&D Analogy

How Corporations Insure Innovation

Large corporations create internal captives to insure their R&D divisions. When a business unit experiments with new products or processes, the parent company's captive absorbs the fortuitous risks of innovation—protecting the unit's P&L from unexpected setbacks while encouraging bold experimentation.

How We Apply This to GCs

Our captive treats each GC like a corporate business unit entering a new product line. By paying premiums into the captive, GCs gain protection against the learning-curve risks of prefab specialization—smoothing cash flow and enabling them to invest confidently in new installation techniques.

Cash Flow Smoothing

Predictable premium payments replace unpredictable out-of-pocket losses. GCs can budget for insurance costs rather than absorbing random claim shocks that disrupt operations.

Learning Curve Protection

New prefab techniques carry inherent risks during the adoption phase. The captive absorbs fortuitous failures while GCs build expertise, reducing the financial penalty for innovation.

Collective Risk Pooling

12 GCs sharing risk means no single contractor bears catastrophic losses alone. The pool's diversity across markets and geographies stabilizes outcomes for all members.

How GC Innovation Insurance Works

Join the Captive

GC commits to prefab specialization and becomes a captive member with ownership stake.

Pay Premiums

$50K annual base premium (adjusted for experience) provides predictable, budgetable costs.

Innovate Confidently

Adopt new prefab techniques knowing fortuitous risks are covered—focus on execution, not fear.

Share in Success

Good loss experience benefits all members through lower future premiums and potential dividends.

Covered Innovation Risks (Fortuitous Only)

- Unforeseen installation complications with new prefab systems

- Equipment failures during technique adoption

- Subcontractor errors on novel installation methods

- Material compatibility issues discovered on-site

- Unexpected code interpretation differences

- Weather impacts on new assembly processes

- Supply chain disruptions for specialized components

- Third-party delays affecting new workflows

Note: Speculative risks (market changes, business decisions, intentional acts) are expressly excluded. Coverage applies only to fortuitous events.

Home Gap Coverage

Like auto gap insurance—but for your ADU/prefab project. Protects buyers and builders from the cost delta between quoted and actual installation costs caused by fortuitous events.

- Covers unforeseen site conditions, supply chain disruptions, utility complications

- Up to 35% gap coverage on baseline project cost

- Fortuitous risk only—speculative risk excluded

Protected Cell Company (PCC)

As the captive grows, GC consortiums and property owners can create their own "cells"—legally segregated compartments with isolated assets and liabilities—beneath the Integral Mass umbrella.

Key Performance Indicators

Risk Coverage

The captive provides comprehensive coverage for three primary risk categories:

Construction Defects

- Structural integrity issues

- Material defects

- Installation errors

- Code compliance failures

Utility Integration

- Water connection failures

- Electrical system issues

- Gas line problems

- Septic system failures

Schedule Delays

- GC availability constraints

- Supply chain disruptions

- Weather delays

- Permit processing

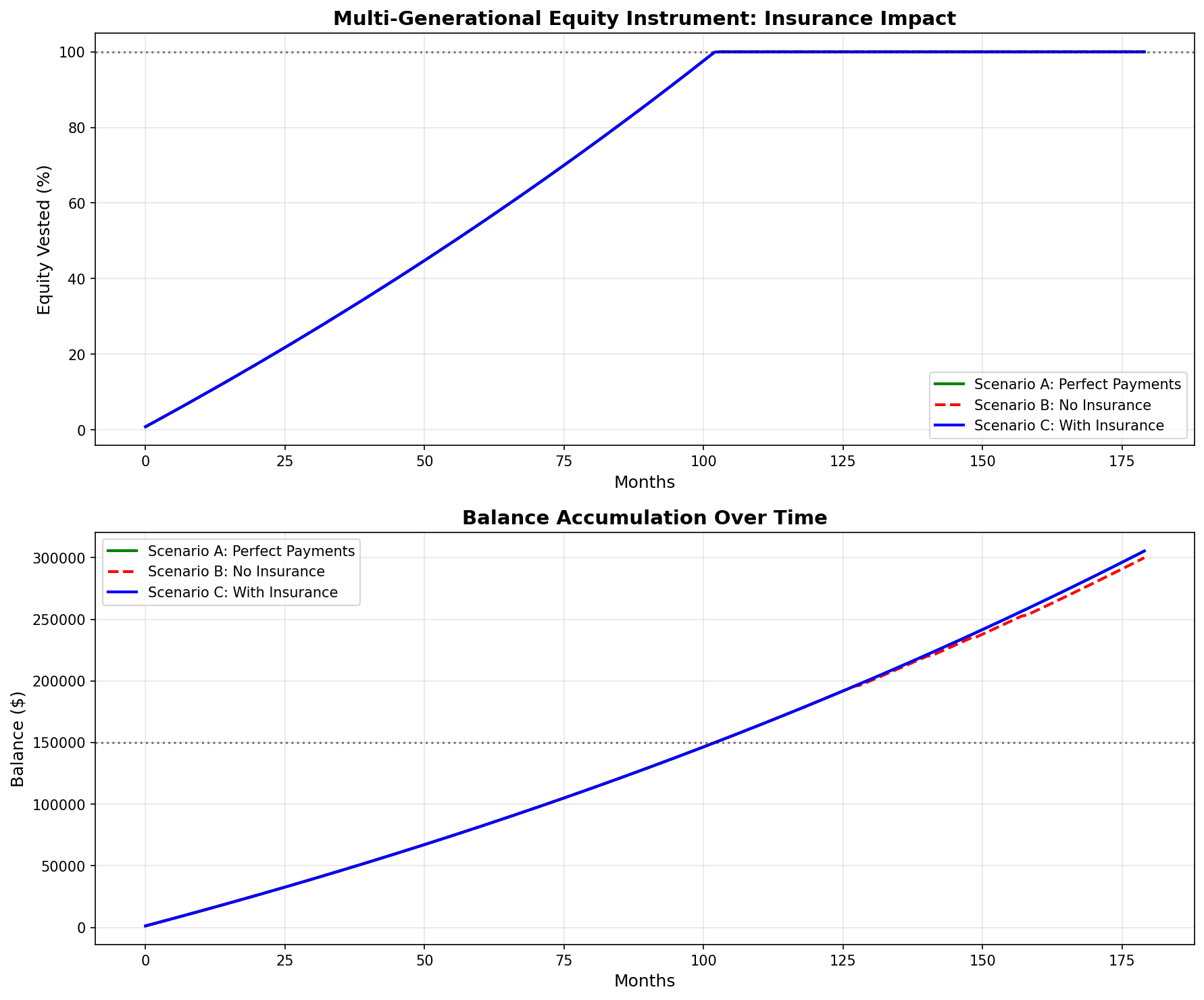

The Multi-Generational Innovation

Rent-to-Equity Financial Instrument

Our unique multi-generational housing model creates a financial instrument where:

- Parents invest in an accessible ADU (Accessory Dwelling Unit)

- Children pay rent that accumulates with interest

- Equity transfers to the child over time

- Residence swap occurs when parents need accessibility features

This structure mitigates vacancy risk and default risk, reducing long-term claim probability for the captive.

Ready to Review the Data?

Explore our comprehensive simulation results and regulatory compliance documentation.